In the United States, a limited liability company (LLC) is a popular business structure that offers owners protection from personal liability for the company’s debts and liabilities. LLCs are hybrid entities that combine characteristics of both corporations and partnerships or sole proprietorships. While the limited liability feature is similar to that of a corporation, the availability of flow-through taxation to the members of an LLC is a feature of a partnership rather than an LLC.

Understanding a Limited Liability Company (LLC)

Limited liability companies are permitted under state statutes, and the regulations governing them vary from state to state. LLC owners are generally called members. Many states allow anyone to be a member of an LLC, including individuals, corporations, foreigners, foreign entities, and even other LLCs. However, banks and insurance companies are notable exceptions and cannot form LLCs.

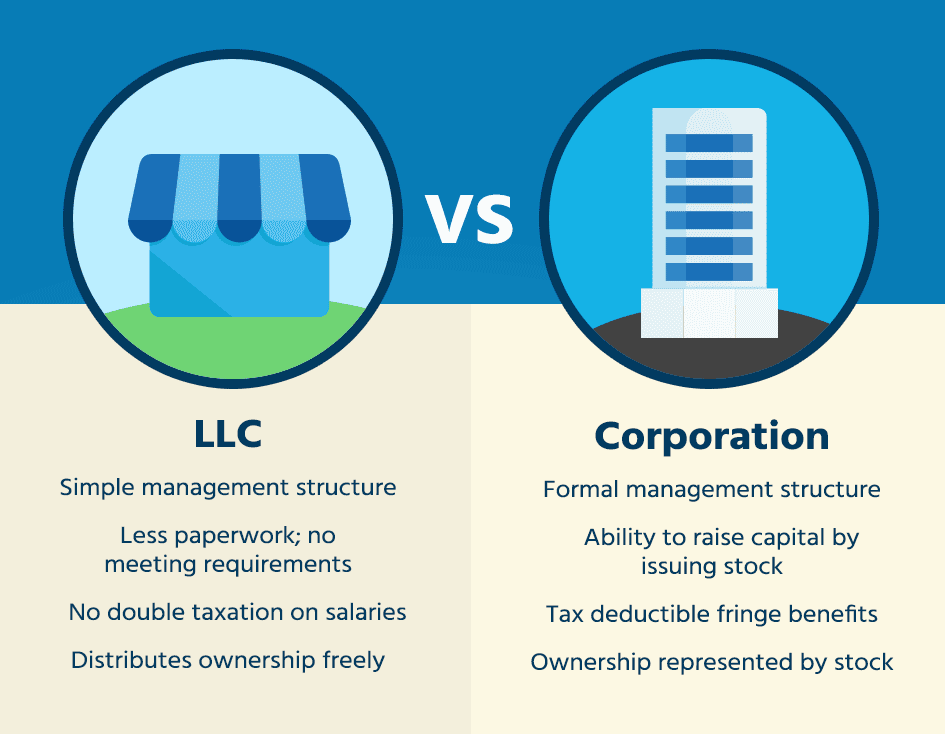

Forming an LLC is relatively easy compared to setting up a corporation, and it offers more flexibility and protection for investors. LLCs may elect not to pay federal taxes directly, as their profits and losses are reported on the personal tax returns of the owners. However, if fraud is detected or if a company fails to meet its legal and reporting requirements, creditors may be able to go after the members.

It is important not to confuse LLCs with Unlimited Liability Corporations (ULCs), which are corporate structures allowed in certain countries and some Canadian provinces. Unlike ULCs, LLCs provide limited liability protection to their owners.

Forming an LLC

The requirements for forming an LLC vary by state, but there are some commonalities. The first step is to choose a name for the LLC. Once the name is chosen, articles of organization must be documented and filed with the state. These articles establish the rights, powers, duties, liabilities, and other obligations of each member of the LLC. The articles of organization also include information such as the names and addresses of the LLC’s members, the name of the LLC’s registered agent, and the business’ statement of purpose.

After filing the articles of organization and paying the required fee to the state, additional paperwork and fees must be submitted at the federal level to obtain an employer identification number (EIN).

Advantages and Disadvantages of LLCs

One of the primary advantages of registering a business as an LLC is the limited personal liability it provides to owners, partners, or investors. By forming an LLC, owners can protect their personal assets from being pursued in the event of bankruptcy or lawsuits against the company. LLCs are often seen as a blend of partnerships, which offer straightforward business agreements between owners, and corporations, which provide liability protections.

However, LLCs also have some disadvantages. Depending on state law, an LLC may have to be dissolved upon the death or bankruptcy of a member, while corporations can exist in perpetuity. Additionally, if the founder’s ultimate objective is to launch a publicly traded company, an LLC may not be a suitable option.

LLC vs. Partnership

The primary difference between an LLC and a partnership is the separation of business assets from personal assets. LLCs insulate owners from the company’s debts and liabilities, protecting their personal assets. Both LLCs and partnerships allow for the pass-through of profits and the responsibility for paying taxes on them to the owners. Losses incurred by the LLC or partnership can be used to offset other income, but only up to the amount invested.

In an LLC, a business continuation agreement can be used to ensure the smooth transfer of interests when one of the owners leaves or dies. Without such an agreement in place, the remaining partners must dissolve the LLC and create a new one.

What Is a Limited Liability Company?

A limited liability company, commonly known as an LLC, is a type of business structure frequently used in the United States. It combines features of both corporations and partnerships. LLCs provide owners with limited liability, protecting their personal assets in case of business failure or lawsuits. Additionally, LLCs allow all profits to be passed directly to owners and taxed as personal income, avoiding double taxation.

What Are Limited Liability Companies (LLCs) Used for?

LLCs are commonly used for various purposes. The main advantages of forming an LLC include protecting owners from personal responsibility for the company’s debts and liabilities and avoiding double taxation. LLCs are utilized by both large and small businesses. For example, Alphabet (Google’s parent company), PepsiCo Inc., Exxon Mobil Corp., and Johnson & Johnson are all LLCs. Additionally, many physicians’ groups are registered as LLCs to protect individual doctors from personal liability for medical malpractice awards.

Are Limited Liability Companies Taxed Differently Than Corporations?

Yes, limited liability companies are taxed differently than corporations. In a corporation, profits are first taxed at the corporate level and then taxed again when distributed to shareholders, resulting in double taxation. LLCs, on the other hand, allow profits to be passed directly to owners, who are taxed only once as part of their personal income.

The Bottom Line

Limited liability companies (LLCs) offer important legal structures for businesses, protecting owners’ personal assets from the company’s debts and liabilities. LLCs also provide beneficial features such as simplified taxation and a straightforward establishment process. Due to these advantages, LLCs are the most common type of business structure in the United States.